Biotech Letter

In Biotech We Trust Especially If It’s This Quiet Riser

While driving back from a three-day biotech conference, I got a call from an old friend who runs a major healthcare hedge fund in New York. He was looking for new ideas after taking a beating on some pharma shorts that went sideways during the recent market rally.

“What’s worth buying in biotech these days?” he asked, his voice thick with spreadsheet fatigue. “Everything feels either overpriced or riddled with regulatory risk since Trump took office.”

I paused, watching a hawk circle lazily over the highway. After a moment, I told him about Regeneron Pharmaceuticals (REGN), a name that had quietly climbed my watchlist.

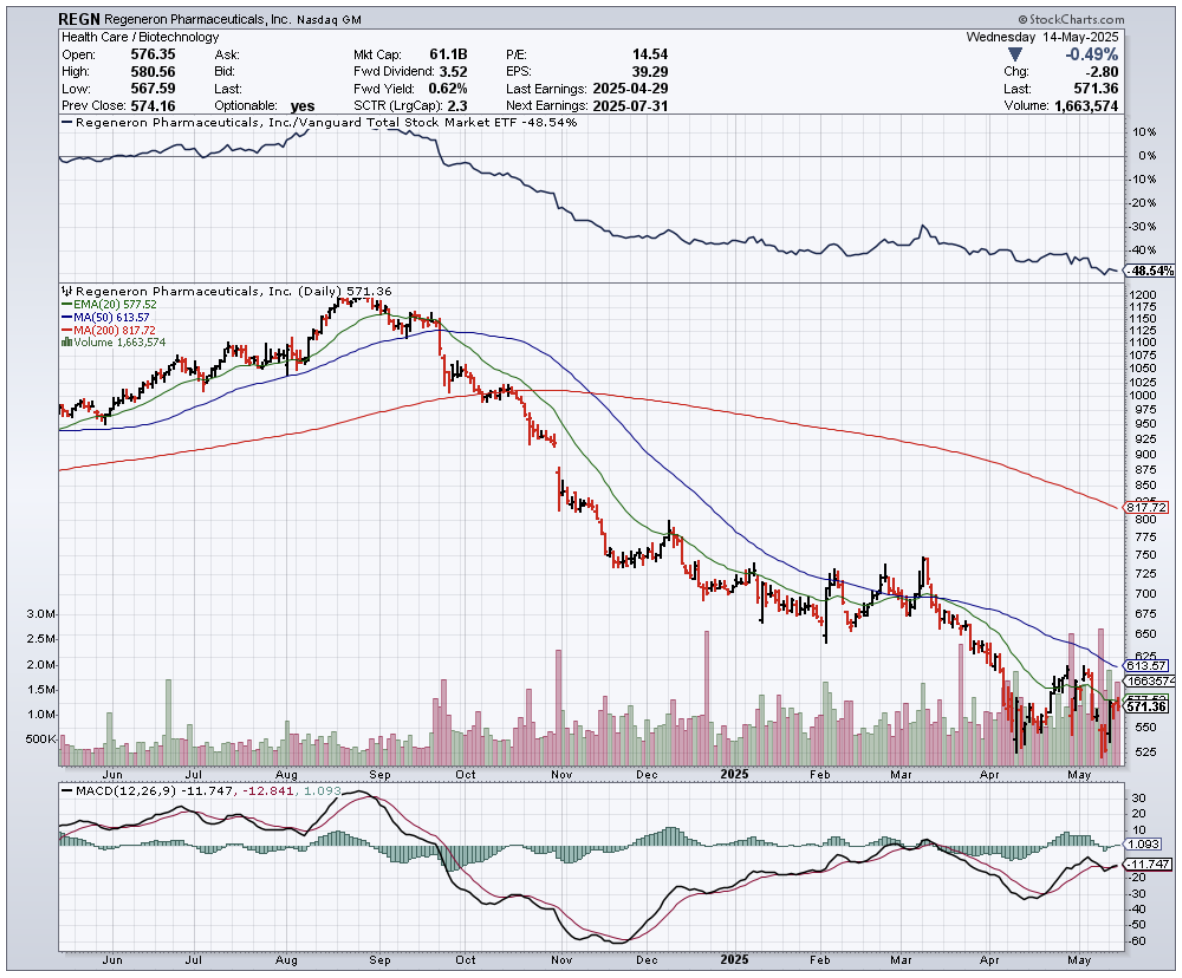

Trading at around $575, Regeneron has been building one of the most formidable drug pipelines in the industry, all while keeping its balance sheet squeaky clean. Their debt-to-equity ratio? A feather-light 0.06. That’s practically Amish in an industry addicted to leverage.

The pipeline stretches across oncology, immunology, hematology, and rare diseases, with recent approvals and submissions pointing to a company firing on all cylinders.

Dupixent, their blockbuster for eczema, continues its climb with 20% year-over-year revenue growth and over $3.6 billion in global sales.

Libtayo and Praluent are making solid showings as well. What’s less well-known is just how global this operation has become: 11 FDA-approved meds in the U.S., 9 by the European Medicines Agency, and 7 in Japan.

That kind of geographic spread gives Regeneron a regulatory hedge others lack.

Even the dividend crowd has reason to peek over the fence. Regeneron started paying a dividend in February. Sure, the 0.67% yield won’t turn heads, but with a payout ratio under 2%, there’s runway if management wants to sweeten the pot.

Meanwhile, the stock’s forward P/E ratio sits at 17.59, a notch below sector average and suggesting the market hasn’t quite caught on.

Of course, it’s not all blue skies and eczema relief. The company is currently fending off a federal case alleging it overcharged Medicare for its eye drug Eylea. That’s a headache, no doubt, but in this industry, litigation is as common as lab coats.

More interesting is Regeneron’s move to double its U.S. manufacturing footprint, investing over $7 billion in facilities in New York and North Carolina. That’s not just expansion — it’s a bet on American-made drugs becoming more politically and economically advantageous in the coming years.

After four days of caffeinated number-crunching, I pegged a three-year average price target gain of 39%, based on reasonable EPS growth and valuation multiples. The stock has taken a hit lately and now trades roughly 36% below its 200-day moving average, nearing its five-year low. For long-term investors, that’s a value signal flashing like neon.

This reminds me of a healthcare panel in Davos a few years back, where someone said the next generation of biotech winners would be those who could navigate regulation while staying financially disciplined. That line stuck with me. Regeneron checks both boxes.

When I laid all this out, my friend was silent for a beat. Then: “So you’re telling me there’s a biotech company with almost no debt, growing revenues, and trading at a discount?”

“That’s exactly what I’m telling you,” I said, pulling into a rest stop. “Sometimes the market actually hands you a gift.”

He laughed. “I’ll have my team dig in tomorrow.”

And me? I’ll be watching Regeneron’s clinical trials as they unfold. In a sector where a single failed drug can end careers, Regeneron’s diversified pipeline and fortress balance sheet offer something rare: a margin of safety.

If this tariff-fueled, policy-shifting biotech landscape continues to evolve, companies like Regeneron — those already leaning into American manufacturing — could find themselves not just surviving, but thriving.